Michael Bruno May 20, 2020

If you like the cadre of big aerospace and defense companies now, you are going to love them later. Among the major trends the novel coronavirus is expected to catalyze within aerospace and defense (A&D) manufacturing is that the big will get bigger by gobbling up others or taking back more work.

In the next few years, vertical integration should pick up momentum, according to several executives and consultants. After decades of OEMs, primes and top-tier companies outsourcing major work on their programs, many see the pendulum swinging back to bringing more of it in-house.

“We've already seen signs of more vertical integration coming through the industry and potentially where some of that could be accelerated as we work through the crisis,” says one advisor.

Boeing started this a few years ago as it insourced avionics and other niche segments. Major consolidation picked up last year with the mergers of Raytheon and United Technologies Corp. and L3 Technologies and Harris Corp. Now, whether it be protecting profits or securing supply, the reasons to own more of the work are burgeoning as industry is refashioned in the COVID-19 crisis.

For starters, aerospace suppliers are facing diminished economies of scale but a greater share of fixed-cost in production, with a likely loss in profitability and competitiveness, say Roland Berger advisors Robert Thomson and Manfred Hader. So-called organic top-line increases, through insourcing and acquisition of additional work packages, are possible but only to a limited degree. A fixed-cost reduction likewise is only feasible up to a certain level due to equipment and overhead structures. So consolidation is an important lever to consider.

Part and parcel to that will be the financial distress into which suppliers in Tier 2 and below fall—and the opportunity to roll them up.

Top CEOs are watching. Speaking May 13 to an investor conference, Honeywell International Chairman, CEO and President Darius Adamczyk cited an inflection point. “For a couple of years now, I've been talking about how it is a seller's market, not a buyer's market,” he told Goldman Sachs. “But that calculus may change in the second half of the year, and I think it could become a bit more of a buyer's market, and the valuations may be better and different. That's something that we want to partake in.”

Feeding the phenomenon could be a desire to bring supply closer to home, both for reliability and geopolitical reasons. Suppliers overseas once were revered for their low-cost footprint, but suddenly they are seen as vulnerable to pandemics, economic stress and global trade wars. In turn, consultants expect industry leaders to take another look at favoring local regions.

Even in the defense realm, which for now is considered safer during this downturn, there is talk of larger firms becoming even more powerful. “Large pure-plays should come through the pandemic relatively unscathed but may be looking at lower spending growth outlooks,” Capital Alpha Partners Managing Director Byron Callan noted May 13. “Mergers and acquisitions may thus be more important in delivering growth—even though it's not organic growth—in 2021-25.”

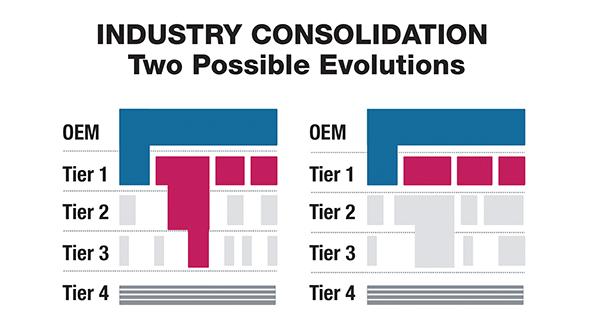

So where to look for vertical integration and consolidation from the top? Clues are already emerging, according to advisor presentations. First, look at niches where top suppliers already are prevalent—environmental and flight-control systems, landing gear, electrical power and interiors—and others where they are not there yet, including maintenance, repair and overhaul, logistics, aerostructures and engines.

Next, look at the supply base from the perspective of a top supplier. Who is distressed or drawing down credit lines? What revenue mix do certain potential targets have—e.g., commercial vs. defense, products vs. services or aging vs. next-generation platforms?

Finally, consider where the new nucleus of consolidation will be. Will more “super Tier 1s” such as Raytheon Technologies emerge, or will conglomeration occur among Tier 2 and 3 providers? The first would allow rationalization of capacity for detailed part production from Tier 1 to 3, for instance, with the super Tier 1s able to secure through-value-chain control and prevent subtier supplier failure, according to Roland Berger. The latter likely would be opportunistically driven rather than following any overarching industry logic.

For smaller suppliers, the questions are more concise, as one consultant says. Do you want to be a buyer, a seller or risk it as is? A simpler question, for sure, but no less difficult to answer.

https://aviationweek.com/aerospace/manufacturing-supply-chain/manufacturing-reshapes-after-covid-19-size-will-matter